Medicare Supplemental Insurance: As per a report given by American Association for Medicare Supplement Insurance, there are more than 14 million people in the United States that had joined with Medigap and have Medicare Supplement insurance, as of 2018. With these numbers, you can guess how many individuals must have joined with Medigap on today’s date.

Many of you must have heard about Medigap, but if you are hearing it for the first time then here are all the necessary details that you must be looking for about Medigap.

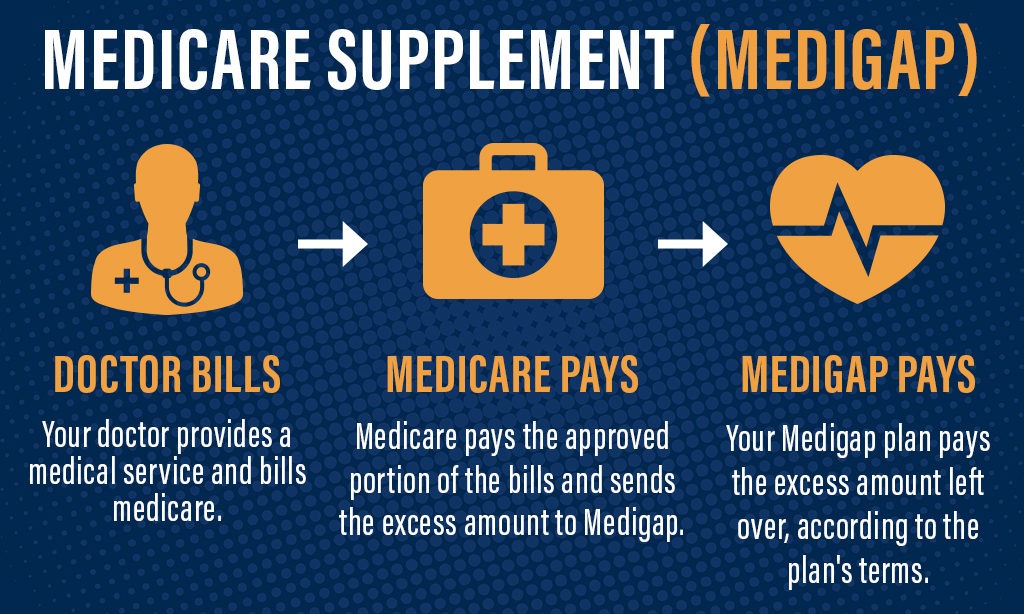

Medigap Overview

Medigap, which is also known by other names such as Medicare supplement insurance or Medicare supplemental insurance, is basically private health companies’ plans that have been sold to supplement Medicare in the U.S. Medigap is sold by private companies in order to help in covering the original Medicare costs, like co-payments, co-insurance, ambulance, doctor charges, among many more.

The best part about Medigap is that it even covers your emergency medical fees in some cases when you are not present in the United States and are traveling outside the country. However, the policy of Medigap only helps in paying you out after you as well as the Medicare have paid the costs of your medical services share.

Overall, there is a total number of ten Medigap Plans that are available currently and those are A, B, C, D, F, G, K, L, M, and N. Additionally, there are also some Medigap plans that are no longer available for the sale to the enrollees who are new Medicare. Such kind of plans consists of C, F, E, H, I, and J. On the other hand, if you are already having one of these plans then you are eligible for keeping it.

Medigap Plans: What’s Covered?

There are many Medigap Plans that differ based on the different factors like copayment types, coinsurance, as well as additional medical fees.

If Medigap Plans Don’t Cover all, it at least covers some portion of it such as:

- It covers Medicare Part A coinsurance as well as the fees of the hospital

- The plans cover Medicare Part A hospital coinsurance or else the co-payment costs

- The plan also covers Medicare Part B coinsurance or co-payment costs

- It also covers blood transfusion costs of the initial three pints

In addition to the above-listed Offers, Some of the Medigap Plans Also Cover:

- It covers the costs of skilled nursing services

- The plan covers Medicare Part A deductible and also Medicare Part B deductible

- It covers Medicare Part B extra charges

- The plan covers emergency medical costs even if you are in a foreign country for travel

What Does Medigap Not Cover?

Medigap policies are basically Health Insurances that cover genuine medical care. It does not cover any additional policy. On the other hand, Medigap policies can cover some of your medical expenses but the things that it does not covers are:

- The prescribed medicines/drugs

- It does not cover the aid of the ear, eyes, or smile that is VHD (Vision, Hearing & Dental) care.

- It does not provide any other medical advantages such as fitness membership or expenses on transportation.

People in or above the 65 age group often ask for these services. As these are not covered by Medigap Policies, old age people can avail these medical services by adding a Medicare Part D plan or can choose the Medicare Advantage Part C plan.

Tip For Choosing A Medigap Plan

If you are availing of Medigap Policies for your loved one then here are some tips that you should consider before choosing the plan.

- Medigap Policies are expensive, so, you must consider a policy that has more coverage over the money.

- If you require Skilled nursing or Hospice service for your loved one then you should pay attention to the policies before choosing.

- You can avail the policy in which during an emergency, your loved one can be transferred to a foreign country to avail yourself of good services.

How Are Medigap Plans Priced?

There are many factors that affect the Pricing of the Medigap Plans for different groups. The rating of the place determines the pricing of your premium plans.

- Community Rated: This kind of plan pricing is not determined by your age. It’ll charge you the same monthly cost regardless of your age. Its pricing is not fixed. It may vary or get influenced due to some other factors like inflation but will never on the age factor.

- Issue Age Rated: This policy is age-friendly. The age of the available person determines the pricing of this plan. The older the person, the lower will be the price of the plan. It will be very less expensive if you are very old to avail of it.

- Attained Age Rated: This Policy focuses on the old age group of people. Its pricing is also determined by the age factor. Unlike the Issue Age Rated Policy, this one gets expensive for older people. It means the older you are, the more expensive this policy will be for you.

- Another factor determining the price of the plans: There are only Four States that offer Medicare facilities to Medigap policies. So, if you are already having a medical condition and you are in another state apart from these 4, then you’ll have to pay a higher premium for your Medigap policies.

Medigap: When to Enroll?

There are many time periods in which you can enroll yourself in the Medicare Premium Plans. Adding Medigap policies to your plan is quite tricky because it has a certain period to do so.

So, here are the time periods in which you can add the Medigap Policies to your plans:

Initial Enrollment Period: You can avail or apply for Medicare Plan and on top of it, you can add Medigap policy. You can add Medigap Policy in between 3 months from your 65th Birth Month & 3 months after your 65th Birth month.

Open Enrollment Period: This is for people who have missed the Initial Enrollment Period. They can apply for Part B if they are about to turn 65. They can enroll for Medigap Policies until 6 months after turning 65.

Well, the Insurance Companies are not supposed to sell you Medigap Policies if you are below the age of 65. You should avail of Medigap Policy as soon as possible because once enrollment is missed; it is difficult to find an insurance company with such good plans.